May 14th, 2026 Options Outlook

Hot inflation

Good Morning! After a hot PPI print and the beginning of the China-US summit, SPX advanced another .6%.

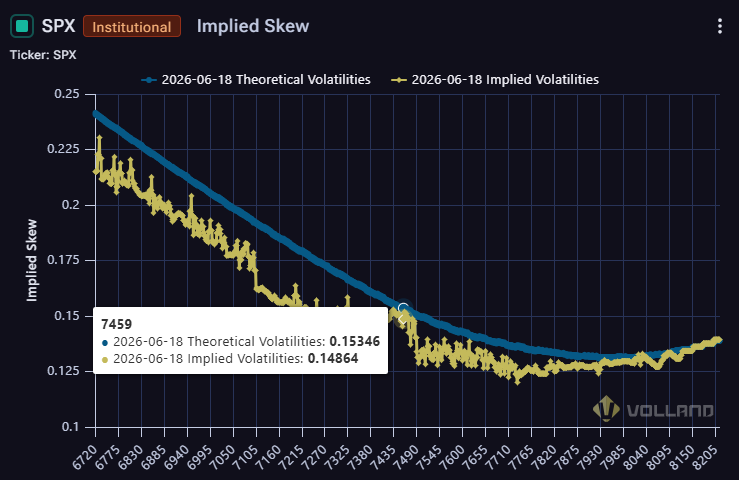

Currently, SPX sits at +18% since the March lows, and +6% from previous all-time highs. Almost all of this is fueled by AI, as the tech independent measures of the market have not even reached their all-time highs. One thing that is intriguing is the relative decoupling of VIX from SPX in this advance. VIX has been relatively stable, matching levels from April 17th when SPX advanced 5.5%. It isn’t like VIX is low either, implying an average of a little more than a 1% daily move. Realized vol has been a bit lower than that, and yet VIX persists in this area. Is skew over priced?

With VIX sustaining so high, June implied skew is below market skew. I think this is because customers have essentially refused to trade their June options during this timeframe.

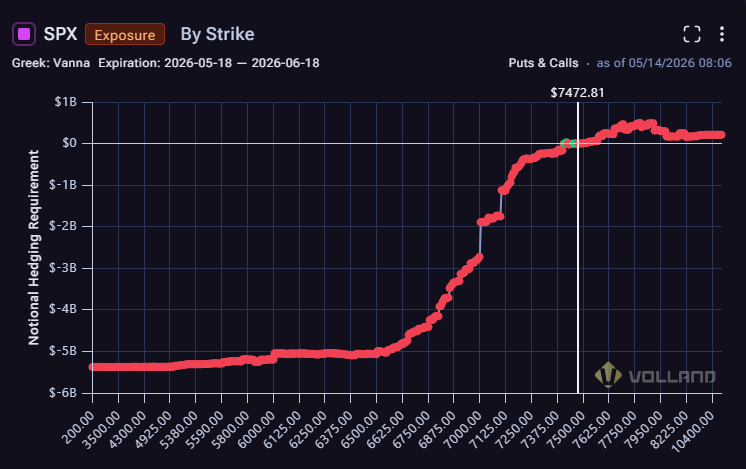

June negative vanna is now at -$5.5B. With IV elevated, what needs to happen is customers need to buy options below spot to support this rally. In the 7100 and below strikes, vanna is negative and IV is too high. That supports a drop. As IV drops in a negative vanna environment, that supports selling by dealers. Vanna wouldn’t get positive until the 6960 area in the June expiries. This is complicated by weekly hedging in puts and sold calls. Before the June expiry, we are looking at +$700M in aggregate vanna. I am still expecting a drop, but it might initially be a rocky drop instead of an elevator until closer to the June expiration.